TL;DR:

- Luxury car asset protection combines tailored insurance, strategic ownership, and expert maintenance to preserve high-end vehicle value.

- In 2026, specialized agreed value insurance, LLC and trust structures, and meticulous preservation are essential, as standard policies fall short.

Luxury car asset protection is the combination of tailored insurance, strategic ownership structuring, and expert maintenance designed to preserve the value and mitigate risks of high-end vehicles. In 2026, this integrated approach has become more pressing as premiums rise, legal frameworks grow more complex, and vehicle values fluctuate. Owners of Ferrari, Lamborghini, Rolls-Royce, and similar marques face risks that standard auto policies simply do not cover. Providers like Chubb have built entire product lines around this gap. Understanding how insurance, legal structures, and physical preservation work together is the foundation of any sound protection strategy.

What specialized insurance options protect luxury vehicles best in 2026?

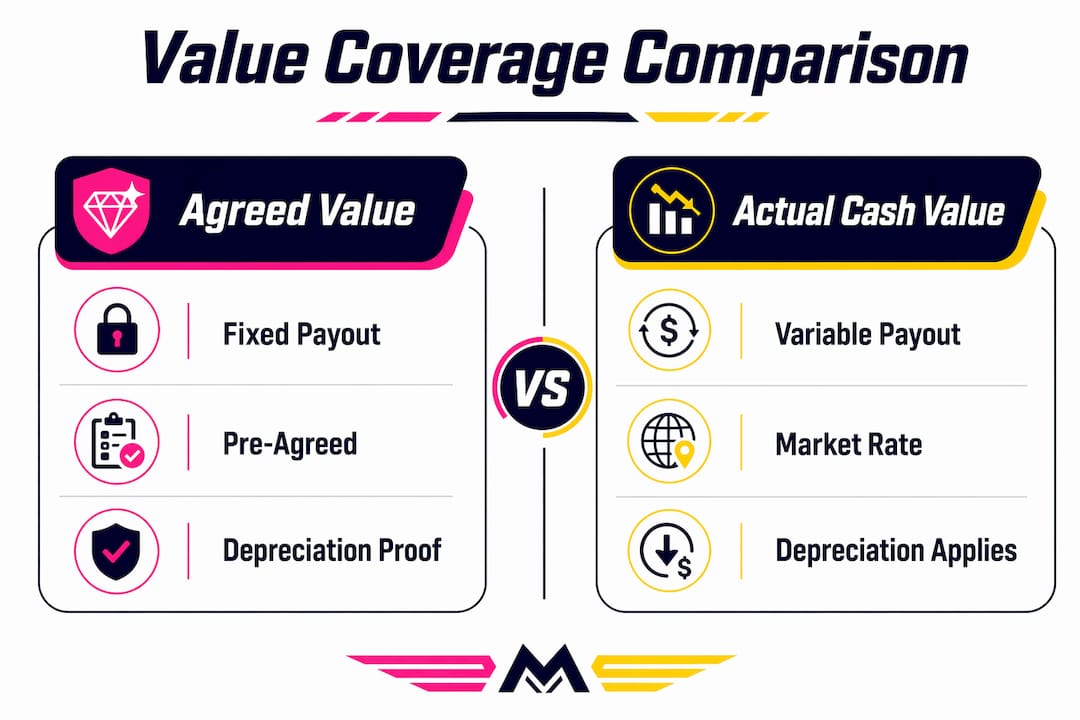

Standard auto insurance is structurally inadequate for luxury vehicles. It pays actual cash value upon a total loss, which means depreciation reduces your payout the moment you drive off the lot. For a $250,000 McLaren or a $180,000 Porsche Taycan Turbo S, that gap between what you paid and what a standard insurer pays can reach tens of thousands of dollars within the first year alone.

The industry term for the right alternative is agreed value coverage, and it is the single most important feature to demand in any luxury vehicle insurance policy. Agreed value coverage locks in a fixed payout amount at policy inception, eliminating depreciation loss entirely upon a total loss claim. For collector and exotic vehicles prone to illiquid markets and valuation swings, this distinction is not minor. It is the difference between recovering your asset’s worth and absorbing a five-figure loss.

Agreed value vs. actual cash value: a direct comparison

| Feature | Agreed Value | Actual Cash Value |

|---|---|---|

| Payout on total loss | Fixed, pre-agreed amount | Market value minus depreciation |

| Best for | Exotic, collector, and luxury cars | Standard daily drivers |

| Depreciation impact | None | Significant in years 1 to 3 |

| Premium cost | Higher | Lower |

Luxury car insurance premiums in 2026 run 16% to 18% higher than standard vehicle premiums, with full-coverage annual costs ranging from $2,134 for entry-level luxury to over $10,000 for top exotic models. That spread reflects the real cost of replacing advanced safety systems, carbon fiber body panels, and proprietary electronic modules that standard repair shops cannot service.

Beyond agreed value, the most protective policies include these features:

- OEM parts requirements: Luxury cars require OEM parts and factory-trained technicians to maintain value. Non-OEM repairs reduce resale value and can void manufacturer warranties.

- Worldwide coverage: Critical for owners who transport vehicles to international events or track days in Europe.

- Equivalent loaner vehicles: Chubb’s high-net-worth auto insurance provides a comparable loaner, not a rental economy car, while your vehicle is being repaired.

- High liability limits: Luxury car accidents carry higher litigation risk. Standard liability limits of $100,000 are insufficient for high-net-worth owners.

- Concierge claims service: Chubb assigns a dedicated claims specialist, reducing the friction and delay that standard insurers impose.

Gap insurance deserves specific attention for owners financing new luxury purchases. Gap insurance costs $20 to $40 annually when bundled into a policy, yet it can prevent out-of-pocket losses of up to $30,000 if a new luxury car is totaled in the early ownership years. Dealerships charge $500 or more for the same coverage. Bundling through your insurer is the straightforward choice.

Pro Tip: Shop for bundled, customizable policies through high-net-worth specialists rather than standard carriers. Providers like Chubb, AIG Private Client Group, and PURE Insurance build policies around your specific collection, not a generic vehicle category.

How can ownership structures and legal frameworks enhance high-value vehicle asset protection?

Insurance covers financial loss after an incident. Legal ownership structures prevent personal liability from attaching to you in the first place. These two layers serve different functions, and using only one leaves significant exposure.

The most widely used structure for exotic car asset protection in 2026 involves a combination of a limited liability company (LLC) and a trust, often layered across favorable jurisdictions. Here is how a sound multi-layer framework typically operates:

- Form an LLC in a protective jurisdiction. Nevada and Wyoming LLCs offer strong charging order protections, meaning creditors cannot seize LLC assets directly. South Dakota trusts add an additional layer of statutory protection for the underlying assets held within the LLC.

- Execute a bona fide lease-back agreement. The LLC leases the vehicle back to you as the operator at fair market rent. This is not a formality. Simple LLC ownership without a commercial lease-back lacks liability and audit protection. The lease must reflect an arm’s length commercial agreement to hold up legally.

- List the LLC as the named insured. The commercial policy must cover the LLC as owner and you as operator. Failing to update the insurer creates a coverage gap that can void claims entirely.

- Invoke Graves Amendment protections. The federal Graves Amendment provides liability preemption for vehicle owners leasing commercially, shielding them from vicarious liability claims across all states. This federal preemption applies only when the lease is genuine, the rent reflects fair market value, and commercial insurance is in place.

- Review annually for regulatory changes. The 2026 regulatory environment has seen increased IRS scrutiny of passive LLC vehicle holdings. Without a legitimate lease-back, the IRS may treat the arrangement as a passive holding, triggering audit risk and disallowing business deductions.

“Jurisdiction selection for LLC and trust ownership significantly impacts asset protection strength, with certain states offering more robust statutory safety for exotic cars.” — Exotic Car Trust 2026 Framework

Selecting the right jurisdiction is not a one-size-fits-all decision. South Dakota and Nevada consistently rank as the strongest states for trust and LLC vehicle protection due to their favorable statutes, low administrative costs, and established case law supporting asset protection structures.

What role do maintenance and preservation practices play in protecting luxury car assets?

Physical preservation is the third pillar of premium auto asset protection, and it is the one most owners underinvest in relative to its long-term impact on value. A Bentley Continental GT with documented OEM service history and an intact factory finish commands a meaningfully higher resale price than an identical model with deferred maintenance and paint correction work.

The core maintenance priorities for protecting high-end vehicles in 2026 are:

- OEM service compliance: Use factory-trained technicians and manufacturer-approved parts at every service interval. This preserves warranty eligibility and supports resale value documentation.

- Environmental damage prevention: UV exposure, acid rain, road salt, and industrial fallout degrade paint and clear coat progressively. A structured environmental protection plan addresses these threats before they compound.

- Surface protection systems: Ceramic coatings and paint protection film (PPF) are the two primary tools. Liquid PPF offers a self-healing, hydrophobic surface layer without the visible edges that traditional film installations sometimes show on complex body lines.

- Documented service records: Every oil change, brake service, and detailing appointment should be logged. Buyers and insurers both assign higher value to vehicles with complete, verifiable histories.

Ceramic coating vs. liquid PPF vs. traditional PPF

| Protection Type | Best For | Key Advantage | Limitation |

|---|---|---|---|

| Ceramic coating | Daily drivers, gloss enhancement | Chemical resistance, hydrophobic layer | Does not absorb impact |

| Liquid PPF | Complex body lines, full coverage | Self-healing, no visible edges | Higher application skill required |

| Traditional PPF | High-impact zones (hood, bumper) | Proven impact resistance | Visible edges on complex curves |

Extended warranties require the same analytical rigor as insurance policies. Extended warranties vary significantly: exclusionary (bumper-to-bumper) plans cover more than stated-component plans, and luxury vehicles require coverage for high-tech electronic modules that cost up to $1,800 per individual repair. Evaluating a warranty on monthly payment alone misses the total contract cost and the specific systems covered.

Pro Tip: Evaluate extended warranty contracts by total cost over the coverage period, not monthly payment. For luxury vehicles, prioritize exclusionary plans that explicitly cover advanced driver assistance systems (ADAS), infotainment modules, and air suspension components.

An elite maintenance checklist built specifically for luxury vehicles covers these systems in sequence, helping owners track service intervals and surface protection renewal timelines without relying on memory.

How do luxury vehicle financing and equity loans contribute to asset protection in 2026?

High-net-worth owners increasingly treat their vehicle collections as liquid collateral rather than static assets. Automobile Collection Financing allows owners to pull 70% to 90% credit against their car collections without selling a single vehicle. Lenders offer up to 90% loan-to-value on certain 1990s modern classics due to stable and appreciating price floors.

The strategic advantages of this approach include:

- Liquidity without liquidation: You retain ownership and use of the vehicle while accessing capital for reinvestment, tax planning, or other asset purchases.

- Portfolio diversification: Equity released from a stable-value Ferrari 550 Maranello or a Porsche 993 can fund positions in other asset classes without triggering a taxable sale event.

- Market timing flexibility: Owners who do not need to sell can wait for peak market conditions rather than accepting below-market offers during downturns.

- Collection-level underwriting: Lenders assess the full collection value, meaning a single lower-value vehicle does not reduce borrowing capacity if the overall portfolio is strong.

The primary risk is overextension. Vehicles used as collateral must maintain their condition and documentation to retain lender-assigned values. A vehicle with deferred maintenance or undocumented repairs can trigger a margin call or a forced revaluation. Preservation practices and financing strategy are directly linked.

What should luxury car owners know about combining all protection layers?

The most common protection failure among luxury car owners is treating insurance, legal structure, and physical preservation as independent decisions. Each layer compensates for gaps in the others, and the combination produces protection that none of the three achieves alone.

A coordinated approach follows this sequence:

- Secure agreed value insurance with OEM repair requirements, worldwide coverage, and concierge claims service through a high-net-worth specialist.

- Establish an LLC and trust structure in a protective jurisdiction, execute a legitimate lease-back agreement, and update your insurer to list the LLC as the named insured.

- Implement a surface protection system appropriate to your vehicle’s use profile, whether that is ceramic coating for a daily driver or liquid PPF for a garage-kept exotic.

- Document everything. Service records, warranty contracts, insurance declarations, and legal agreements should be stored in a single organized file accessible to your attorney and financial advisor.

- Review all policies and legal structures annually. The 2026 regulatory environment, particularly IRS scrutiny of LLC vehicle holdings and state-level insurance rule changes, makes annual review non-negotiable.

Pro Tip: Work with a multi-disciplinary team: a high-net-worth insurance specialist, an asset protection attorney familiar with your state’s LLC statutes, and a preservation professional who understands the specific maintenance requirements of your marque. No single advisor covers all three domains.

High-net-worth car care requires this coordinated approach because the cost of a single gap, whether a denied insurance claim, a pierced LLC veil, or a paint correction job that reduces resale value, consistently exceeds the cost of prevention.

Key takeaways

Luxury car asset protection in 2026 requires agreed value insurance, a legitimate LLC and trust ownership structure, and documented physical preservation working together as a single integrated system.

| Point | Details |

|---|---|

| Agreed value insurance | Locks in a fixed payout, eliminating depreciation loss on total loss claims. |

| LLC and lease-back structure | Requires a bona fide commercial lease to provide liability and audit protection. |

| Surface preservation | Liquid PPF and ceramic coatings protect finish integrity and support resale value. |

| Automobile Collection Financing | Allows 70% to 90% equity access without selling vehicles, preserving collection ownership. |

| Annual review requirement | 2026 IRS scrutiny and insurance rule changes make yearly policy and legal review mandatory. |

What I’ve learned about protecting luxury cars that most advisors won’t tell you

Most conversations about luxury car protection focus on insurance products and stop there. After working with high-value vehicle owners at Mannyceramicprotouch, I’ve seen the pattern clearly: owners who invest in a premium policy but neglect physical preservation end up with a vehicle that is insured for its agreed value but worth less on the open market because the finish has degraded, the service records are incomplete, or the paint shows uncorrected swirl marks from improper detailing.

The uncomfortable reality is that agreed value insurance protects you in a total loss scenario, which is statistically rare. What affects your vehicle’s value every single day is how it is maintained, stored, and protected from environmental damage. A Lamborghini Huracán with a compromised clear coat and no documented service history does not command the same price as an identical car with a ceramic-coated finish and a complete OEM service file, regardless of what the insurance declaration page says.

I’ve also watched owners build sophisticated LLC structures and then undermine them by failing to execute a legitimate lease-back agreement or forgetting to update their insurer. The legal framework only works when every component is in place and maintained. Partial compliance is not compliance.

The owners who protect their assets most effectively treat their vehicles the way institutional collectors treat fine art: with documented provenance, professional preservation, appropriate insurance, and a legal structure that separates the asset from personal liability. That combination, applied consistently, is what actually holds up.

— Emmanuel

Protect your luxury vehicle’s finish with Mannyceramicprotouch

Physical preservation is the layer of protection that works every day, not just when something goes wrong. Mannyceramicprotouch specializes in advanced surface protection for luxury, exotic, and high-value vehicles in Fort Lauderdale, applying Liquid PPF and high-performance ceramic coatings engineered for long-term finish integrity.

Liquid PPF delivers self-healing protection without the visible film edges that traditional PPF installations show on complex body lines. For owners of Porsche, Ferrari, Bentley, and similar marques, the difference in finish quality and long-term value retention is measurable. Explore the Liquid PPF vs traditional PPF comparison to identify the right solution for your vehicle, or contact Mannyceramicprotouch directly to schedule a consultation tailored to your specific model and protection goals.

FAQ

What is luxury car asset protection?

Luxury car asset protection is the integrated use of agreed value insurance, legal ownership structures such as LLCs and trusts, and expert physical preservation to maintain the value and limit the liability exposure of high-end vehicles.

Why is standard auto insurance insufficient for luxury vehicles?

Standard policies pay actual cash value, which factors in depreciation and can leave owners tens of thousands of dollars short on a total loss claim. Specialized programs like Chubb’s high-net-worth auto insurance provide agreed value payouts and OEM repair requirements that standard carriers do not offer.

How does an LLC protect a luxury car owner?

An LLC separates the vehicle from personal assets, limiting liability exposure. For full protection, the LLC must execute a bona fide lease-back agreement at fair market rent and be listed as the named insured on a commercial policy. Without these elements, the structure provides limited legal benefit.

What does Automobile Collection Financing offer luxury car owners?

It allows owners to borrow 70% to 90% of their collection’s value as collateral without selling any vehicles, providing liquidity for reinvestment while retaining full ownership and use of the collection.

Is liquid PPF better than traditional PPF for exotic cars?

Liquid PPF provides self-healing surface protection without visible film edges, making it well-suited for vehicles with complex body lines. Traditional PPF offers proven impact resistance in high-contact zones. The right choice depends on the vehicle’s use profile and the owner’s finish quality priorities.